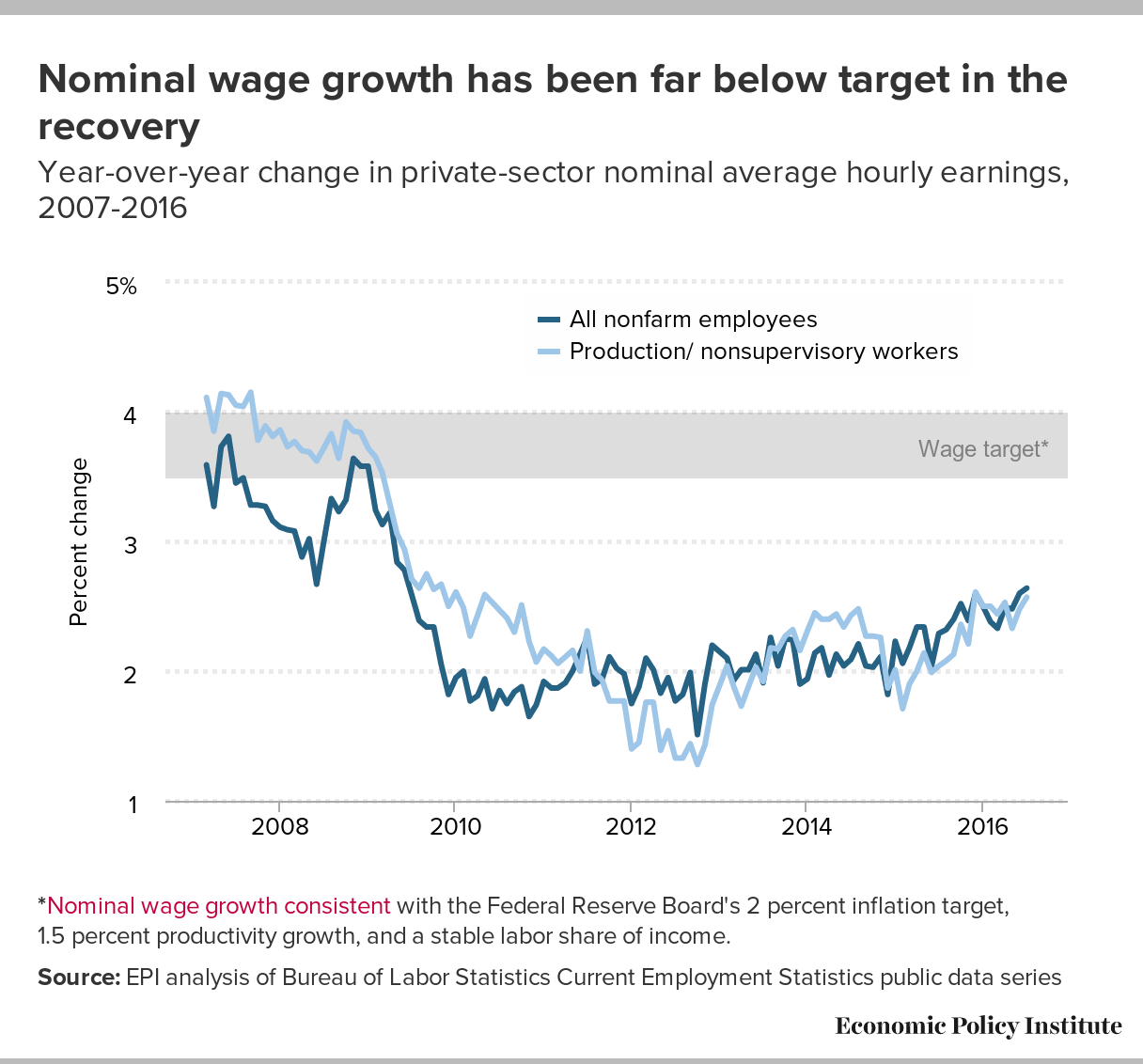

Should we care about slow nominal wage growth when price inflation is slow? YES.

Nominal wages for American workers rose by 2.6 percent in the 12 months ending in December 2015. Over the same time, prices have risen just under 0.7 percent (held down mostly by falling oil prices). This mean that real (that is, inflation-adjusted) wages have grown 1.9 percent in that year. In historical perspective, this is a very healthy rate of real wage growth (for example, real hourly wages for the bottom 70 percent of workers have averaged well under 0.5 percent annually since 1979).

{kind=link}

Since it is this real, not nominal, wage growth that influences living standards, shouldn’t we be perfectly happy with this constellation of wage and price inflation? Not really, for a number a reasons.

For one, the extraordinarily low rates of price inflation won’t continue. They’ve been driven by large declines in commodity prices. The gains to real living standards are genuine—cheap gas really does make paychecks stretch further (though how good cheap gas is in the long run for climate change is a whole other story), but we know that commodity prices are volatile and are likely to stabilize or even rise in the next year. If either of these things happens, the overall rate of inflation in the next year will rise.

Further, even if commodity prices remained depressed forever and overall price inflation really did permanently shift to a slower pace, it is far from clear that this would be a good outcome or that the real wage growth seen in the past year would continue.

Quite soon after any perceived permanent shift towards lower price inflation, nominal wage growth would surely slow. Workers and employers bargain over nominal wages, with an expected rate of price inflation in the background. Recent inflation declines have not been expected so have hence been a windfall to workers, but if inflation really does settle down to a new slower pace for an extended period of time (and if “core” inflation rates—price growth stripping out the effect of food and energy prices—slowed markedly), then workers and employers would realize that slower nominal wage growth would deliver the same real growth they had originally been targeted, and so nominal wage growth would drift downwards. In summary, either the last year of inflation declines have been transitory and will reverse (most likely), or they will be seen by workers and employers as permanent and this will drag down rates of nominal wage growth (less likely).

{kind=link}

Additionally, there is a strong reason to think that policymakers should be aiming for an economy with wage and price inflation significantly faster than what we see today. Say that policymakers want real wages to rise 1.5 percent per year (assuming that this is the trend rate of productivity growth). You could generate this growth with 1.5 percent nominal wage growth and zero inflation, or with 3.5 percent nominal wage growth and 2 percent inflation. Why should we think that the second combination is better?

The simple answer is that higher inflation increases the effectiveness of tools meant to fight recessions and spur faster growth when the economy needs it. To make this concrete, we have just gone through 7 years with zero nominal short-term interest rates as the Federal Reserve has tried to spur recovery from the Great Recession. When the Fed lowers nominal rates, they are trying to induce businesses and households (and governments) to borrow and spend more. But borrowing decisions are made with respect to real interest rates, not nominal. And, the real interest rate is simply the nominal rate minus the rate of price inflation. Think about it—if a friend asks for a loan and offers to pay you 5 percent interest on it, does it matter to you if price inflation is running at zero percent or 10 percent when evaluating this proposal? Of course it does. At 10 percent inflation, a 5 percent interest rate on money you lend would see you losing purchasing power for your trouble.

So, when the Fed sets the nominal short-term interest rate at zero, this provides much more powerful spur to borrow when inflation is at 2 percent than when it is at zero, or (equivalently) when the real interest rate is minus 2 percent versus zero. In the former case, borrowers are actually receiving a negative real interest rate—they’re being paid to borrow.

So if we’re worried that the Fed’s short-term interest rate policy is bound by zero (or at least pretty close to it), this means that it’s better to hit this zero nominal interest rate bound with higher rates of inflation rather than lower. Hitting the next recession with zero percent inflation would be a really, really bad thing.

Finally, in an economy still laden with lots of household debt, faster rates of inflation help erode the real burden of this debt more quickly, which also spurs recovery. Say that you took out a fixed-rate mortgage to buy a house in 2007 with the expectation that the 2.8 percent price inflation of that year would persist. Since your monthly mortgage is fixed in nominal terms, it gets less onerous every year of positive price inflation—and if you assumed 2.8 percent inflation going forward, you expected your mortgage bill to get 2.8 percent less onerous each year. Now that inflation rates have gotten much lower since 2007 (and averaging well under 2 percent each year since 2013), your mortgage payment is significantly more expensive today relative to what you planned it would be in this year back when you originally took on this debt. This more expensive debt payment crowds out possibility for spending on other goods and services, dragging on overall demand growth in the economy when this demand growth is still sorely needed.

All in all, from a short-term living standards perspective, I’m happy workers got a nearly 2 percent pay bump this year, no matter how they got it. From a medium-term perspective of macroeconomic risk, I’m really unhappy with an economy that is generating such low rates of wage and price inflation.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.